Click here to view original web page at rabble.ca

While inflation is slowing down, the Bank of Canada’s steep interest rate hikes don’t have much to do with it.

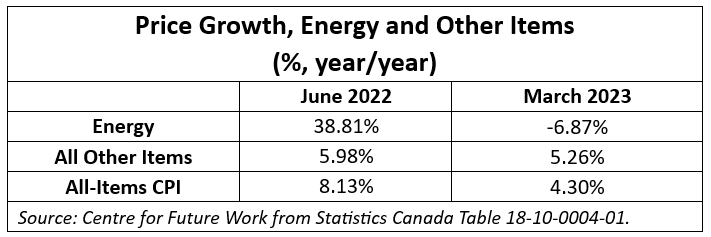

New inflation data indicates a welcome slowing of inflation. Prices increased by an average of 4.3 per cent over the 12 months ending in March. That’s barely half the year-over-year inflation rate just nine months ago, in June 2022 (when inflation peaked at 8.1 per cent).

Despite this encouraging news, however, there are some important and worrying factors lurking in the weeds:

1. Core inflation (excluding food, energy, and other volatile items) is now faster than headline inflation (up 4.5 per cent in the previous year, versus 4.3 per cent for all items). This suggests future risk that inflation could rise – especially if some of the changes in non-core items (and energy, in particular) reverse themselves.

2. Indeed, almost all the slowdown in inflation since June is due to energy. The CPI excluding energy slowed just 0.7 of a percentage point in that time: from 5.98 per cent to 5.26 per cent. In contrast, the headline all-items CPI rate slowed by 3.8 percentage points in the same time. Energy costs were the key factor driving inflation higher before June (not wages and labour costs); and by the same token, the decline in energy costs (and hence overall inflation) since June had nothing to do with painful increases in Canadian interest rates.

WATCH: David Macdonald: Who really benefits from inflation?

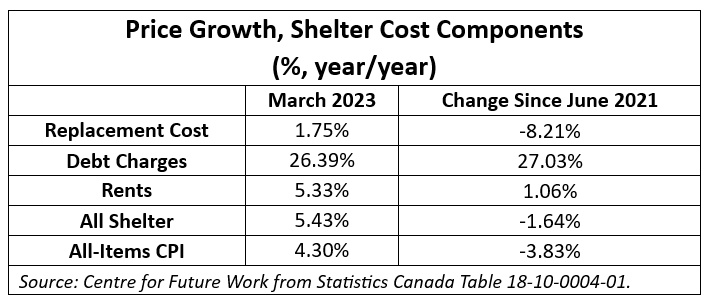

3. Worse yet, shelter costs are now growing faster than the overall rate of inflation – and by the biggest margin in two years. Shelter costs rose 5.43 per cent in the last 12 months, versus 4.3 per cent for overall inflation. Skyrocketing debt service charges (due to higher interest rates) rose by 26 per cent in the last year. That crushing burden more than offset the impact of higher interest rates on real estate prices (known as ‘replacement cost’ in the CPI). Meanwhile, rents are also rising – in part because fewer people can afford a home, with interest rates so high. Ironically, therefore, interest rates are now causing faster inflation, through higher shelter costs.

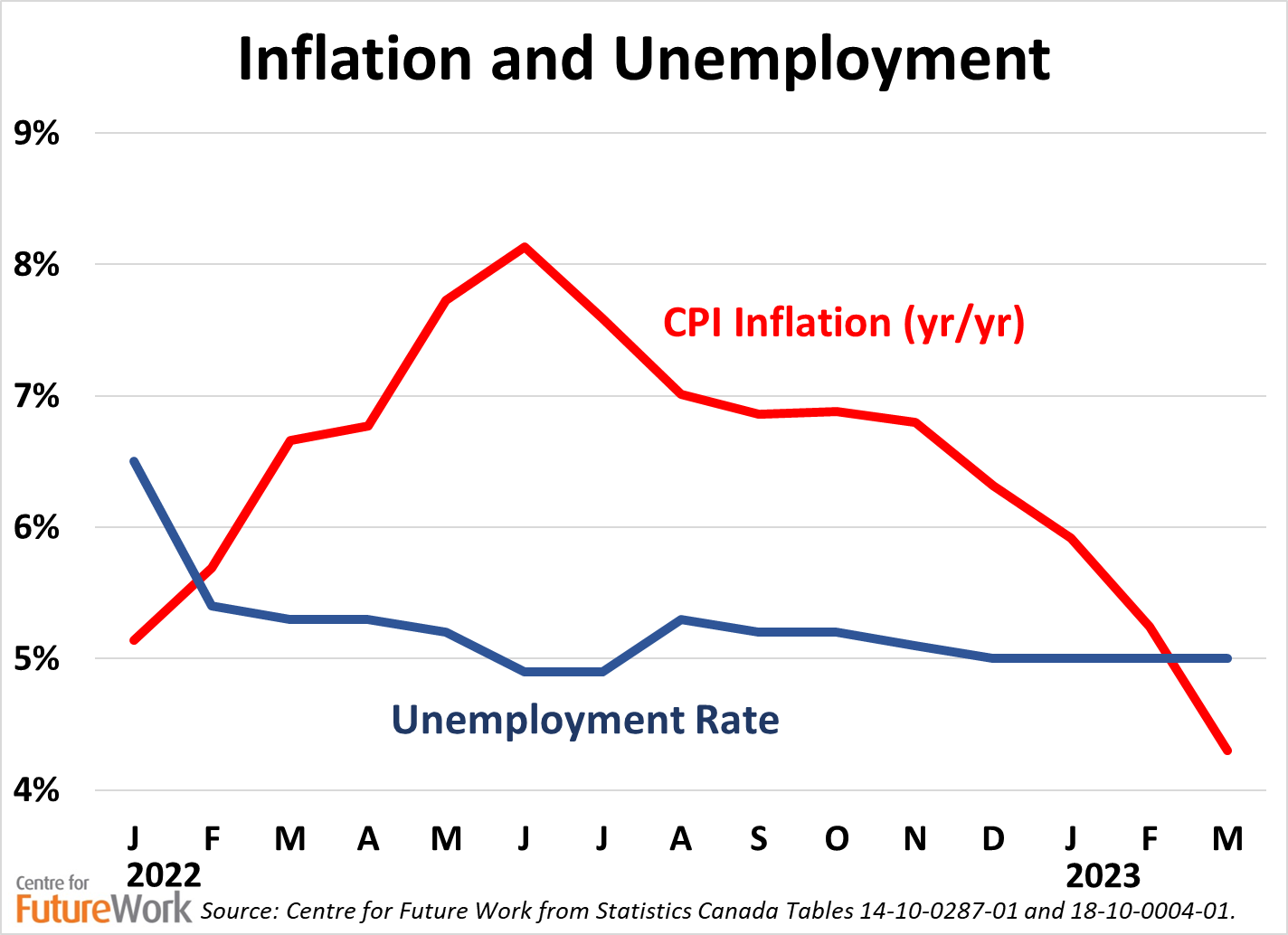

4. Finally, the new inflation data confirm there is no correlation between inflation and unemployment – despite the repeated claims of the Bank of Canada that an “overheated” labour market, and rising wages, is causing inflation. As clear in the following figure, inflation didn’t rise because of lower unemployment. And since June it’s fallen substantially, despite sustained low unemployment. The Bank of Canada’s recommitment to the doctrine of ‘NAIRU’ (Non-Accelerating Inflation Rate of Unemployment, a theory that says unemployment must be kept adequately high to discipline workers and suppress wage growth) is not supported by the actual experience of this inflationary episode.

In sum, it is welcome news that inflation has come down so rapidly. But don’t credit higher domestic interest rates – which are perversely raising inflation, through their impact on shelter costs. Meanwhile, another energy price shock (as could result from oil production cuts recently announced by the OPEC+ cartel) would push inflation back up, in the absence of policies to cap energy prices and redistribute unprecedented petroleum company profits. And even if inflation abates, the Bank of Canada’s re-commitment to orthodox NAIRU-based monetary policy could serve to keep unemployment needlessly high, with resulting economic and social consequences, for years to come.

The experience of the last two years has confirmed that knee-jerk economic theories which automatically blame workers and their wages for any outbreak of inflation need to be discarded. Yes, inflation has been a problem. In this case it clearly resulted from unique and temporary after-effects from the COVID pandemic. Yet the Bank of Canada and other orthodox policy-makers unreflectively targeted labour markets for tough medicine to bring inflation down – even though workers are the victims of this inflation, not its cause.

So while we can celebrate the slowing rate of inflation, and hope that it continues, we cannot let up our demands for fundamental changes in macroeconomic policy – including a recognition of the role of corporate profit-taking in driving the cost of living crisis.